Try our learning program for free!

STEMVentor LMSBlockchain - Part 2: Technology

Vikas Mujumdar, March 20, 2020

In part 1 of this 3-part series on Blockchain, the concept and intent (what business value it can add) of this technology was explained. In part 2, I will explain some of the technical and implementation details, so you can become familiar with how this new technology works under the hood.

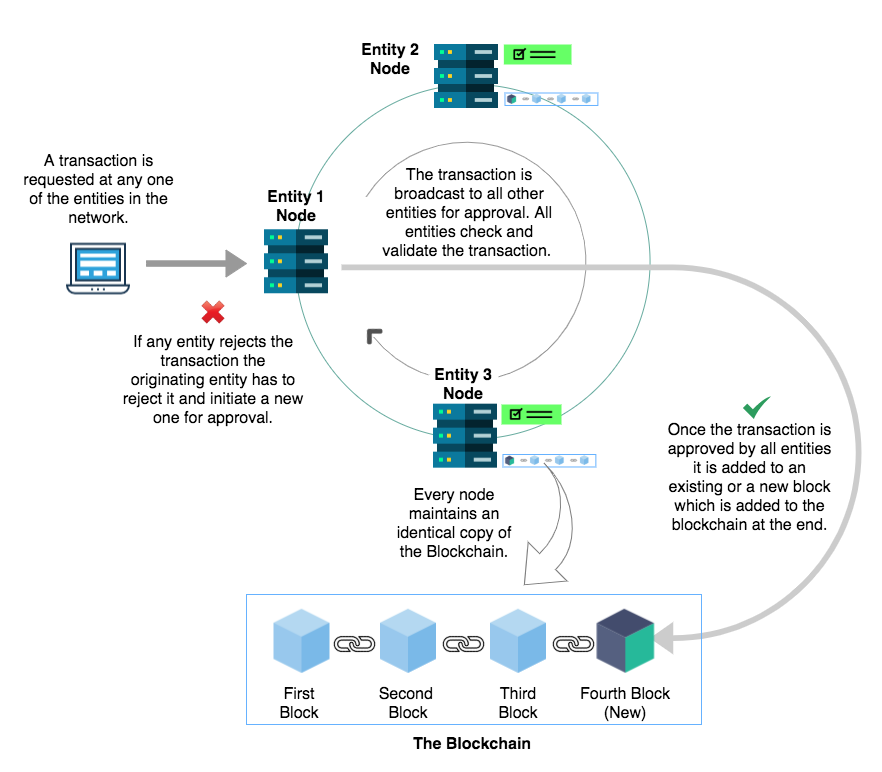

Here's a visual depiction of how a transaction gets recorded in a Blockchain solution:

Credits: Icons made by Freepik from Flaticon

Credits: Icons made by Freepik from Flaticon

Components of a Blockchain Solution

A Blockchain implementation comprises of the following components:

- Nodes: The servers that run the processing algorithms and manage the data are referred to as nodes. Every entity participating in a Blockchain solution must maintain its own node.

The Network: For a Blockchain implementation all participating nodes must be connected together on a data network so that they can exchange data. This could be a private network or the public Internet with appropriate security.

Blocks: Since we are using the reference of a ledger to understand the Blockchain approach, we can consider blocks to be the equivalent of pages in a ledger. Each block stores one or more transactions, just like a page of a ledger. When a block is filled up (each block has a maximum defined data size) a new block is created. Blocks contain an identifier, a timestamp and the transactions.

The Chain: When a new block is created, it is linked to the previous block, to create a chain of blocks. This chain establishes the sequence in which blocks were created and added to the chain. To create the chain, blocks store the previous block identifier. Every node stores a complete copy of the chain, with all the blocks and all their transactions, and this copy is updated at the same time on every node.

Consensus Mechanisms: Consensus mechanisms are protocols that make sure all nodes agree on which transactions are legitimate and are allowed to be added to the blockchain. These consensus mechanisms are crucial for a blockchain in order to function correctly. Any party may submit any transaction to be added to the blockchain, so it’s necessary that all transactions are constantly checked and validated and that the blockchain is constantly audited by all nodes. Without a good consensus mechanisms, blockchains are at risk of inconsistent data and various types of attacks that could compromise your data.

Assurances of a Blockchain Solution

Immutability: This is the characteristic, or feature, of a blockchain to remain unaltered and indelible. All components of a Blockchain implementation including the transactions, blocks and the chain of blocks are all immutable.

Security: Using a combination of the consensus mechanism, encryption with a digital signature and another data-securing mechanism known as hashing, the data on a Blockchain comes with all the properties of a secured transaction. These are authentication – the source or owner of the data can be verified, confidentiality – the data cannot be viewed by anyone not explicitly authorised to do so, integrity – the data cannot be altered or tampered with in any way and non-repudiation – the source or owner of the data cannot claim to have not created the data.

Implementation Challenges

While Blockchain is quite a good solution in theory, there are a few challenges that need to be addressed before it can become a widely used solution for enterprise applications.

Co-operation and Collaboration: The first hurdle to cross in building a multi-entity solution would be to get all the entities to sign on to the solution and all its implementation challenges, investments and process changes. Even with a closed group of partners, such as a manufacturer and its distributors, this may be a challenge, let alone across an open network of competing entities such as banks. One, if not the only, approach would be for a group of large influencers in any industry to form a consortium and define the standards and highlight the benefits to get the others on board.

Complexity: Blockchain solutions are still very complex to build and especially given that they are multi-entity solutions it would take a lot of standardisation of data formats and communication protocols between multiple and possibly disparate systems. The required skills are not yet available to the extent required for large scale deployment and such a solution would impact the core of an enterprise and needs to be designed, implemented and deployed with a high level of knowledge and maturity in the subject.

Speed and Performance: While individual computing power is likely quite sufficient for the processing required for Blockchain solutions, a de-centralised system requires a lot of communication between computers on the network. For example, the nature of the solution requires that all nodes on a network provide their consent to any node wanting to record a transaction. In a live system where near-real-time responses are important – such as banking and trading – the overhead of getting consensus may be prohibitive.

Security: While the Blockchain technology has defined several and reasonably sufficient security controls, possibly stronger than existing centralised systems, the exposure if a Blockchain was indeed hacked into would be to data from the entire network of entities participating, as against from one entity in a traditional in-house system.

Use Cases

There are two popular solutions today that are built on Blockchain. One, Cryptocurrency, is very widely used and the other, Smart Contracts, has a high potential for use in business applications.

A cryptocurrency is a medium of exchange, such as the Indian Rupee, the US dollar or anyone of the many global currencies, but is digital-only. It uses Blockchain as an underlying technology to control the creation of monetary units and to verify the transfer of funds between owners. The best-known cryptocurrency is Bitcoin and actually, Blockchain as a technology and all its design patterns were created to launch Bitcoins.

I will not be getting into any more detail on cryptocurrencies. They are very well-evolved as a technology and in their implementation, and are even widely used in the global markets as an alternate currency for some types of trade. However, the jury is still out on whether or not they should be made legal tender and how should they be regulated and so on, and until that is all sorted out by governments and financial regulators across the world, I personally prefer to stay clear of even discussing them.

In part 3 of this article, I will explain Smart Contracts and explore a use case in the space of logistics to demonstrate how these can add value and increase process efficiency.